Leandro Sanz

Assistant Professor of Finance

Mendoza College of Business, University of Notre Dame

I study corporate finance, with a focus on how firms respond to frictions in capital markets, product markets, and production networks. My recent work examines supply chain risk, intangible assets, and firms’ pricing decisions.

Ph.D. in Finance, The Ohio State University.

Recent

Selected working papers

-

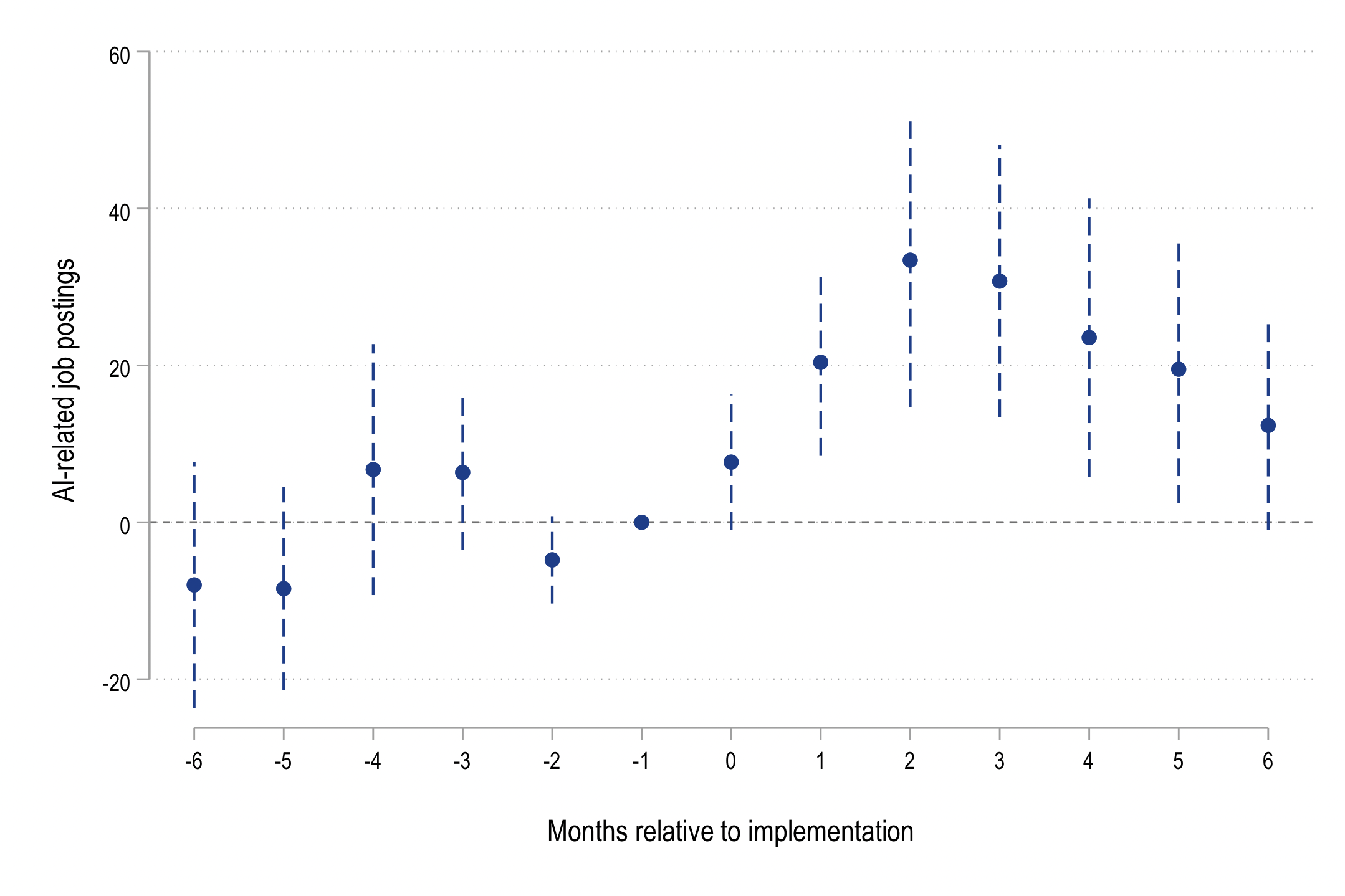

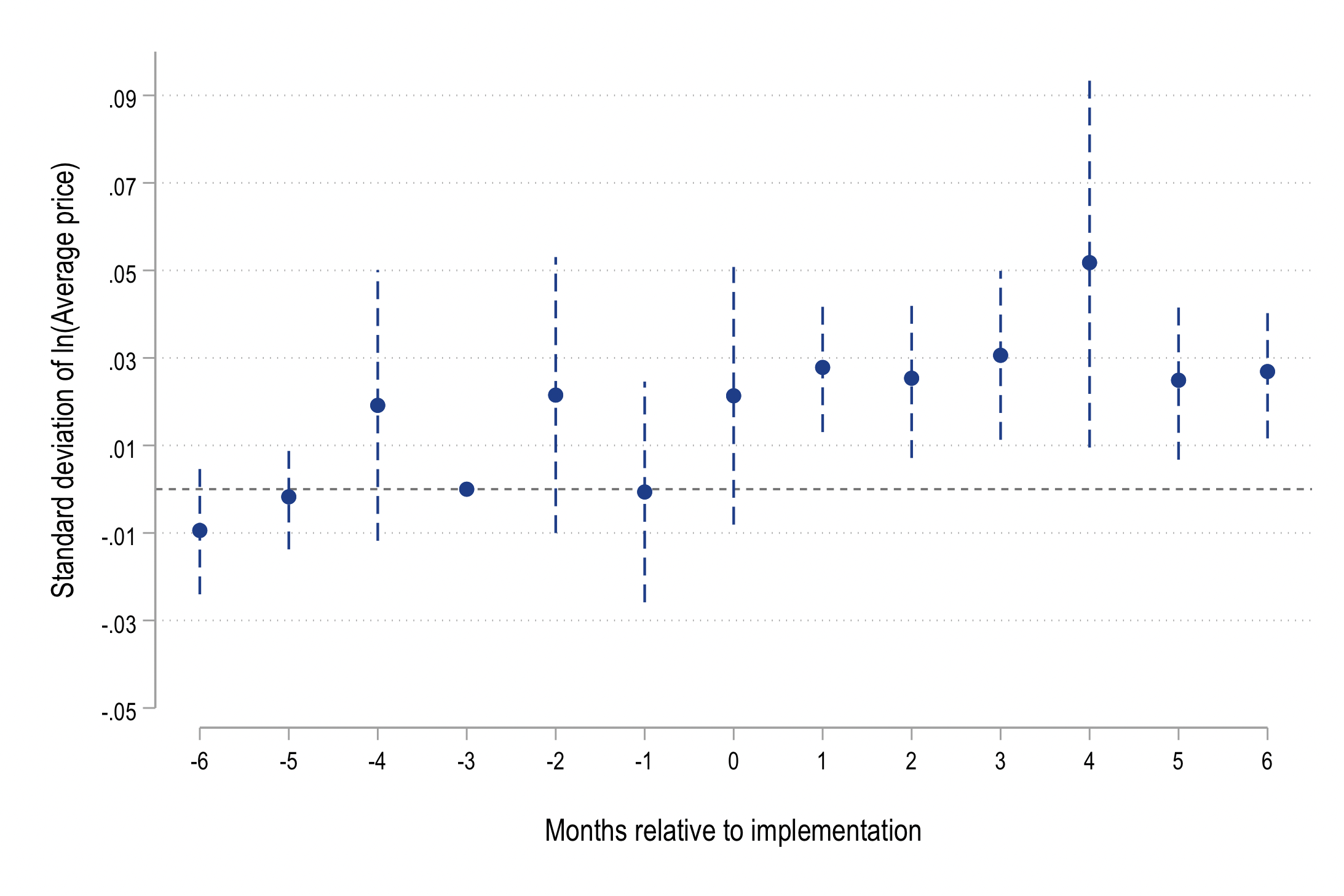

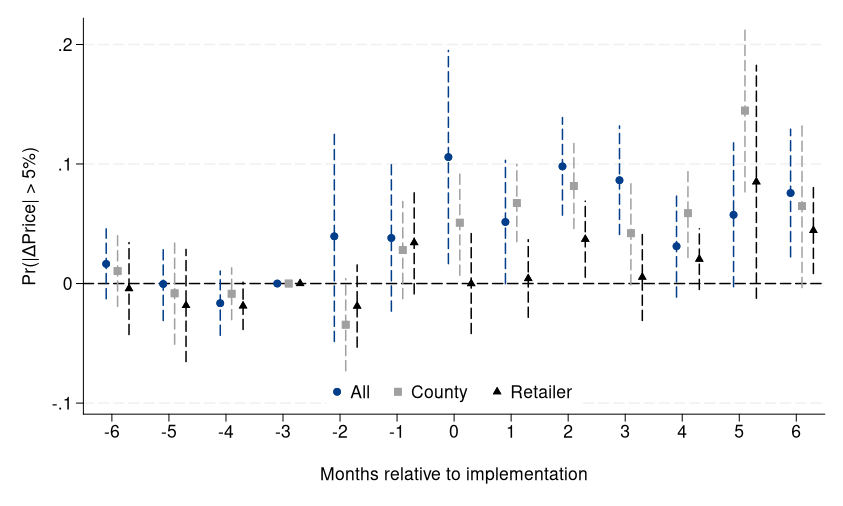

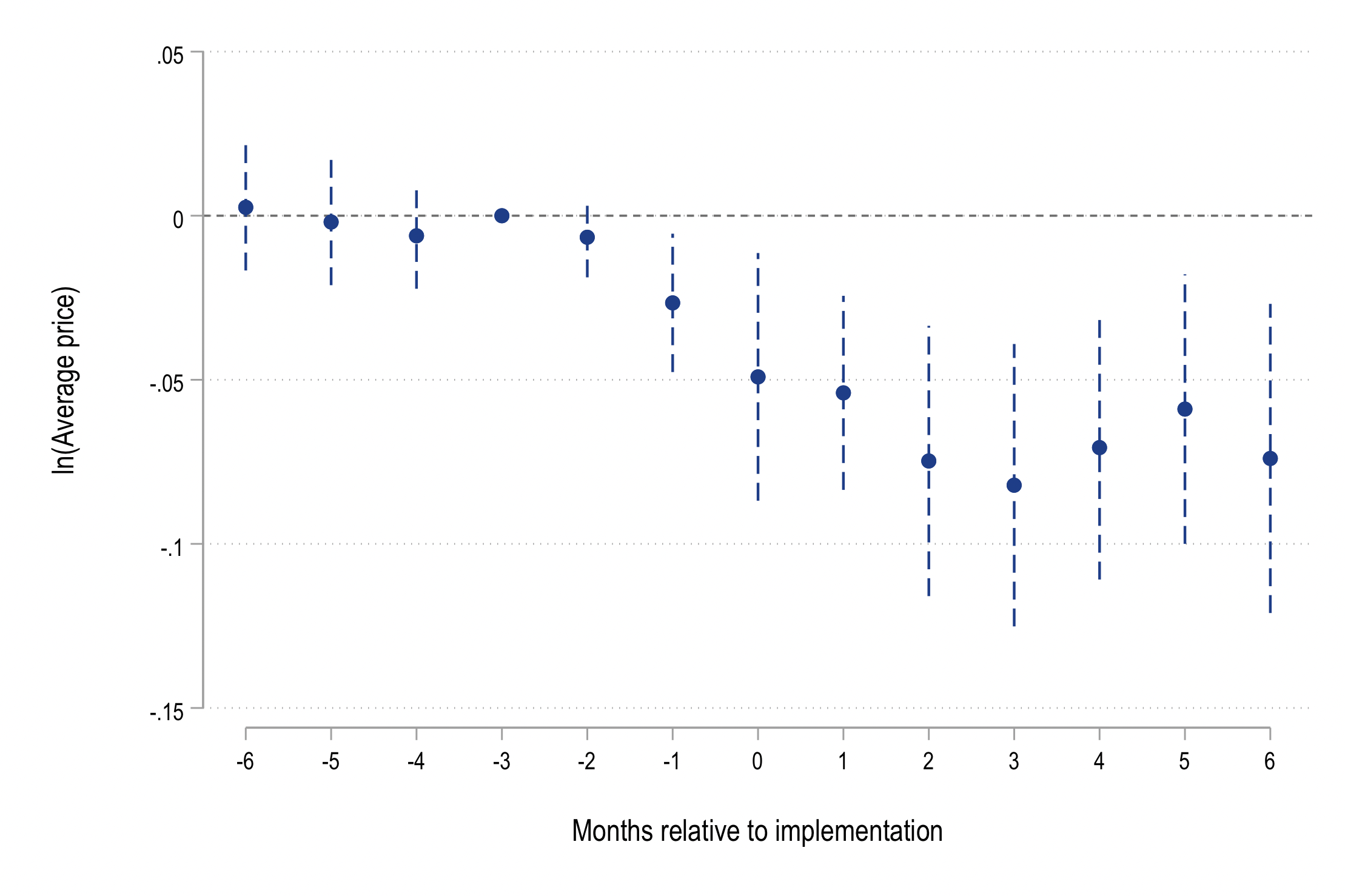

Who Sets the Price? The Vertical Origins of Uniform Pricing

We show that the systematic component of retail price-setting originates primarily upstream with manufacturers, and that AI adoption reduces the upstream information frictions behind uniform pricing.

Abstract. Retail prices in U.S. consumer markets are jointly produced by manufacturers and retailers, but we show that the systematic component of price-setting originates primarily upstream. Using manufacturer-product scanner data spanning approximately 5 billion UPC-store-month observations, we decompose retail price variation into manufacturer and retailer components. Manufacturer identity accounts for approximately 90 percent of explained variation in price levels and 97 percent in price changes. Price dispersion is shaped by both layers of the chain, though manufacturers remain the largest source of explained variation. We show that pricing practices change after brand acquisitions: acquired UPCs converge toward the acquirer's incumbent pricing behavior when the acquirer already operates in the target's category, but diverge from the acquirer's broader pricing behavior in expansionary acquisitions. Private-label products, which compress the manufacturer-retailer information wedge, exhibit greater geographic dispersion and responsiveness to local conditions than national brands. Finally, consistent with a reduction in upstream information frictions, products sold by more AI-exposed manufacturers exhibit greater geographic dispersion, more frequent repricing, and lower prices after the introduction of scalable generative AI APIs, with stronger responsiveness to local conditions. The results indicate that retail pricing rigidities reflect upstream informational frictions that technology can relax, rather than immutable features of retail markets.

AI adoption

Price dispersion

Repricing frequency

Price level -

Organization capital, large startups, and the dearth of IPOs

We show that startups relying heavily on organization capital to achieve scale through digital technologies are more likely to remain private and grow large rather than exit early via IPO or acquisition.

Abstract. Many startups in the 2000s have remained private after achieving large valuations, a pattern that funding availability alone cannot explain. We propose that startups relying heavily on organization capital to achieve economies of scale and network effects through digital technologies are more likely to become large private firms than exit earlier via an IPO or acquisition. Using LinkedIn data, we construct a novel measure of organization capital intensity for startups. Exploiting a legal shock that strengthened organization capital protection, we provide causal evidence that organization-capital-intensive startups are more likely to remain private and grow large rather than exit early.

-

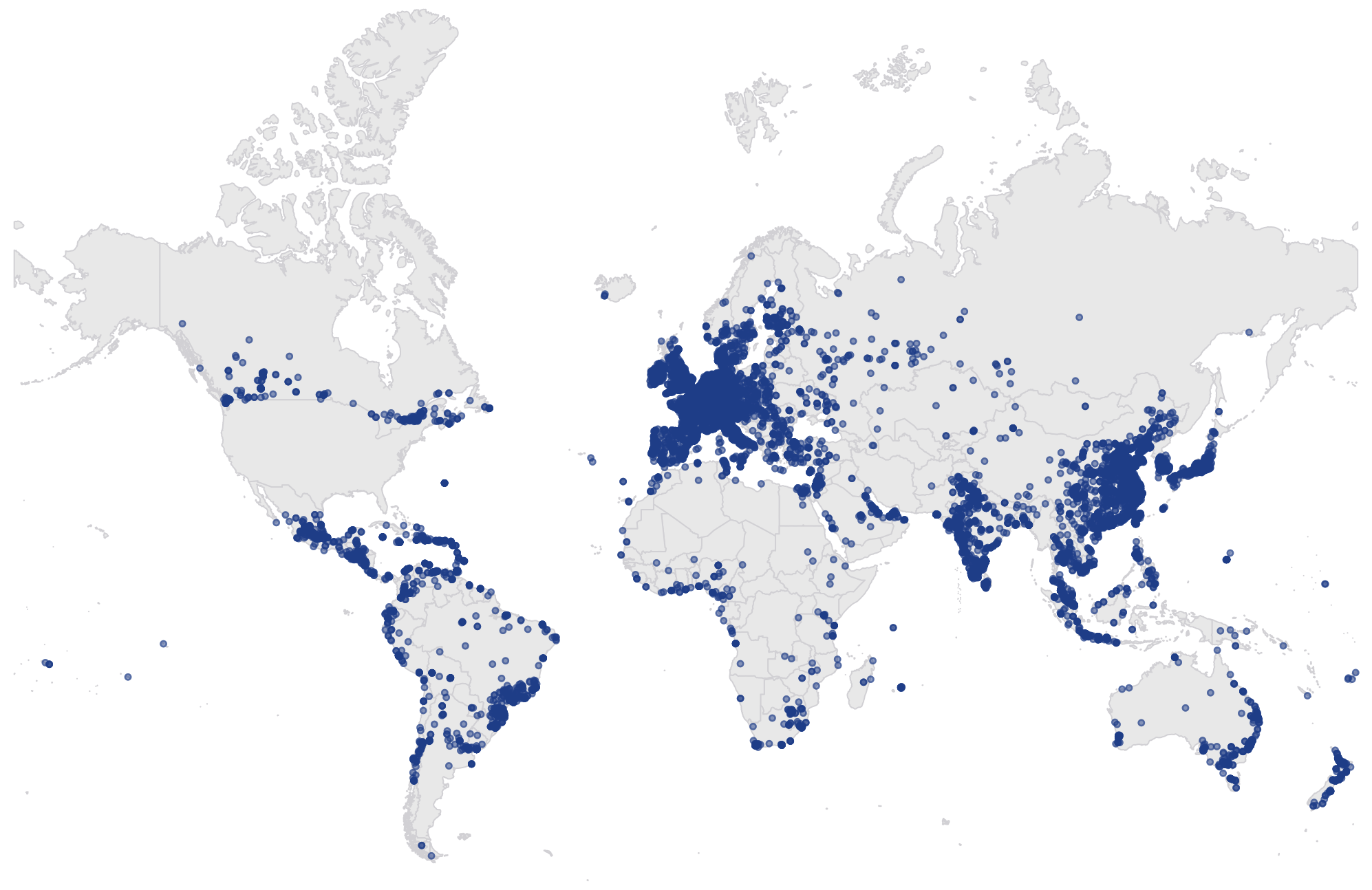

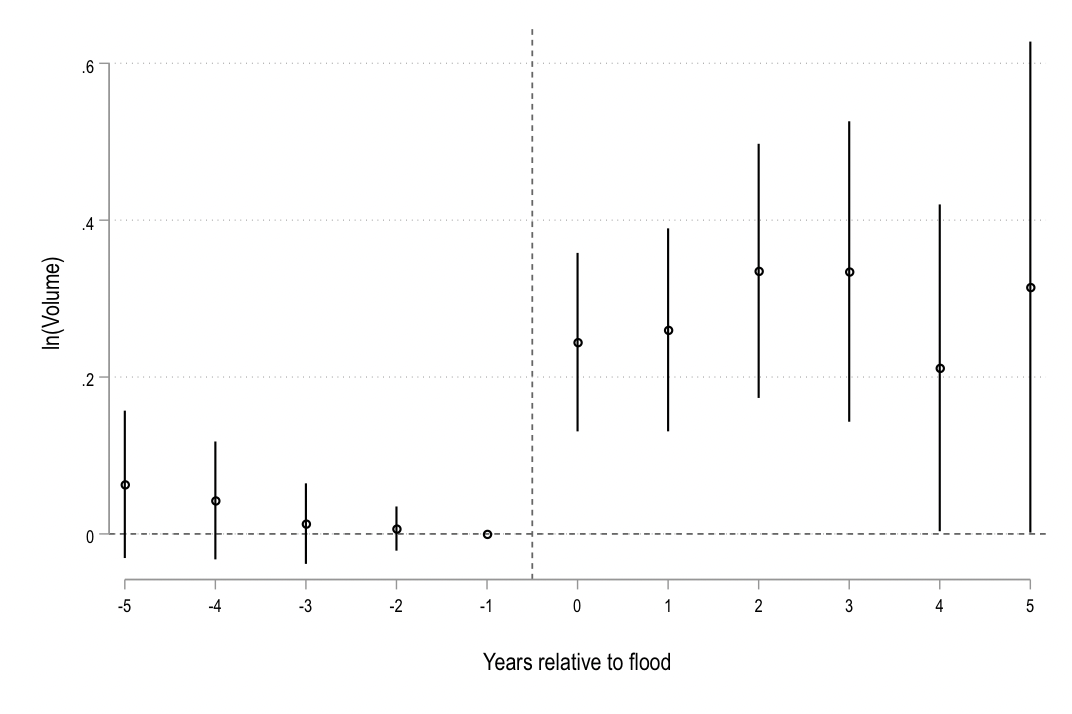

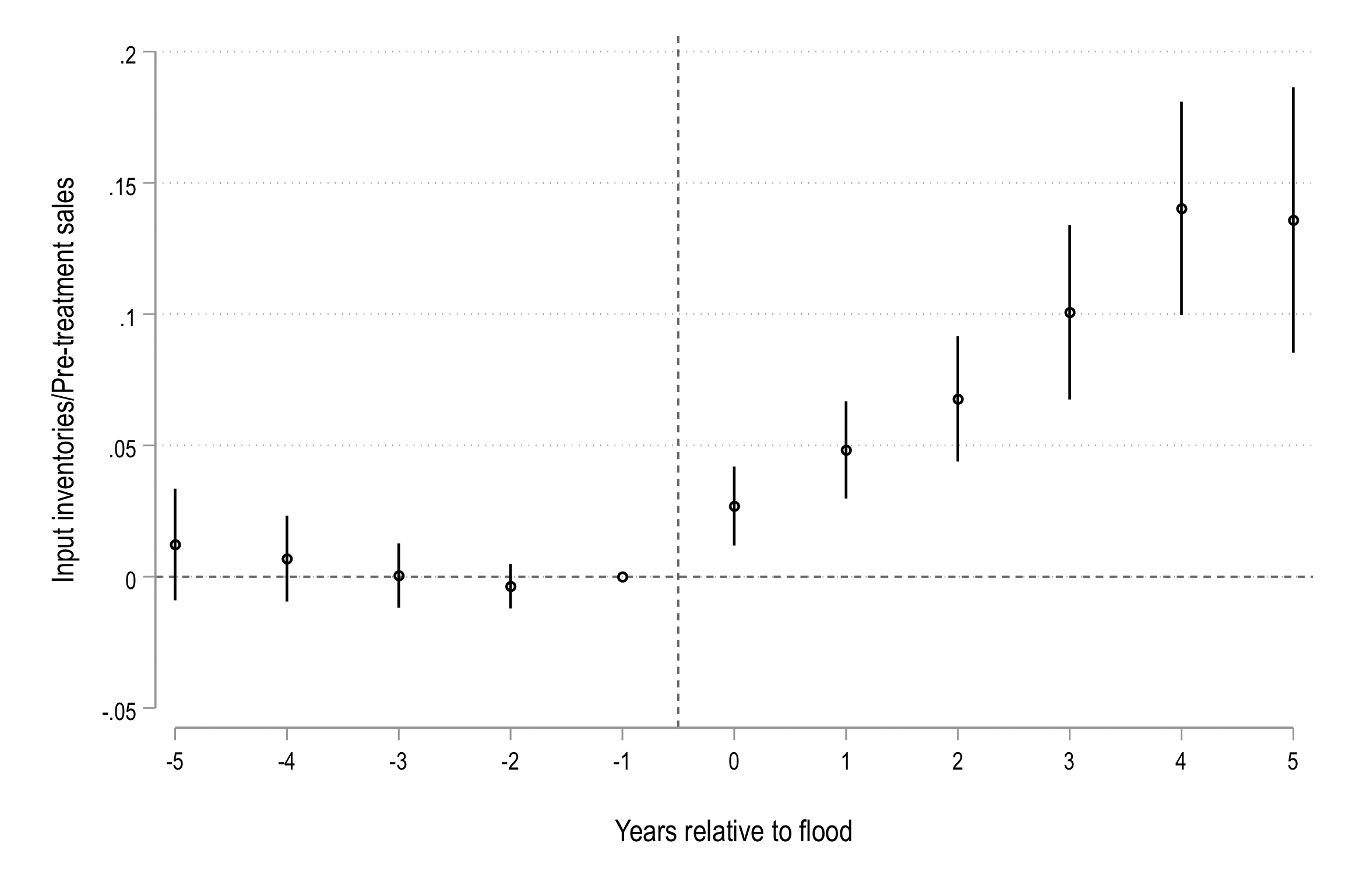

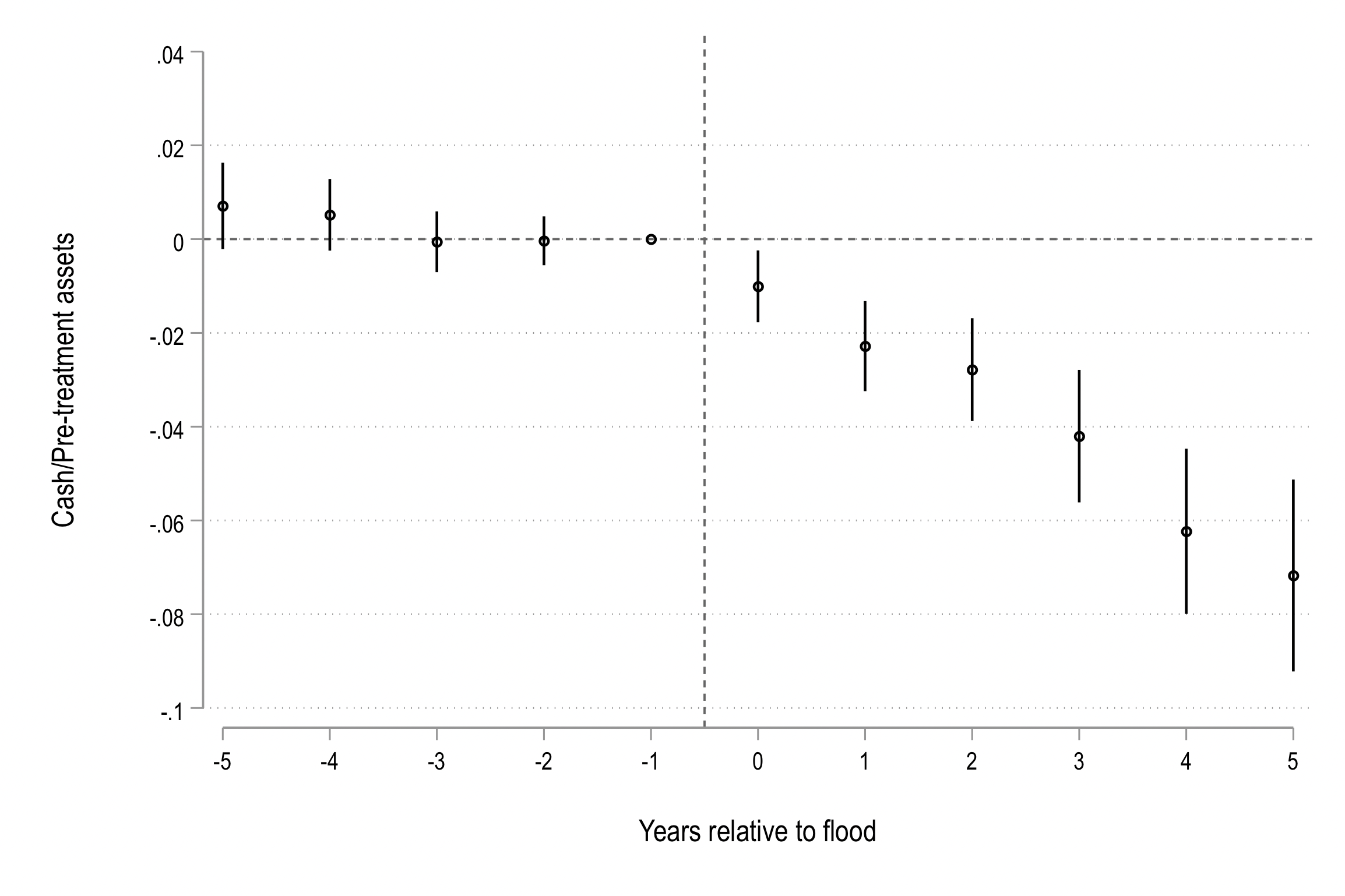

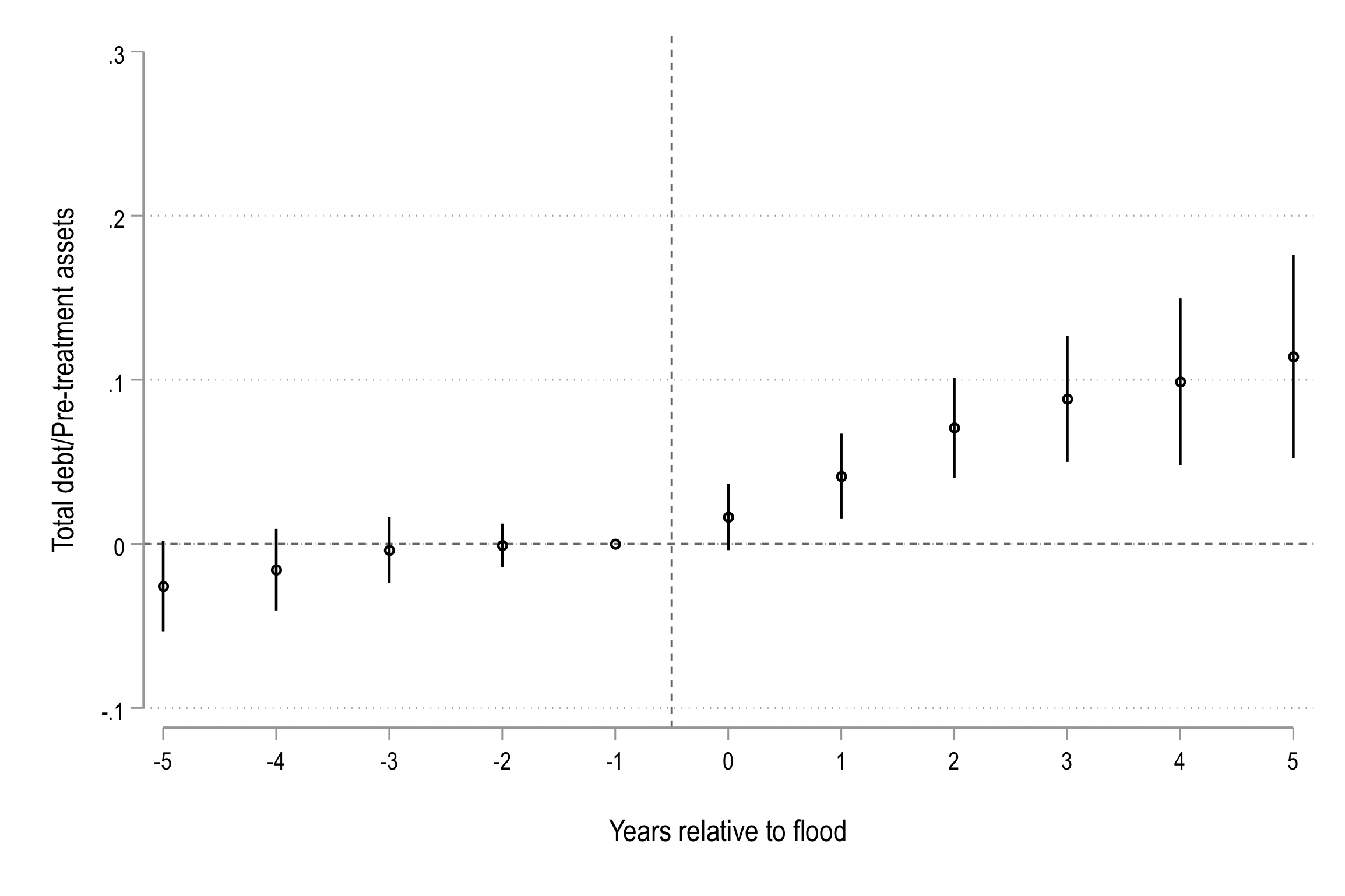

Building Corporate Resilience to Supply Chain Disruptions

I examine how firms build resilience against supply chain disruptions to hard-to-replace inputs. Firms hold more inventory, less cash, and higher leverage, and update these policies after shocks that reveal new information about risk.

Abstract. I examine how exposure to disruption risk from hard-to-replace inputs affects corporate resilience investments and firms' learning about that risk. Using a new dataset on 11,000 foreign suppliers to U.S. manufacturers, I show that firms with fewer alternative suppliers hold more inventory and less cash, and have higher leverage. Exploiting natural disasters that disrupt suppliers, I find that firms update their beliefs about disruption risk and make persistent changes to corporate policies in response. Consistent with learning, the response is strongest after first-time shocks. Finally, firms with higher inventory buffers are better protected against performance losses when disruptions occur.

Supplier map

ln(Volume)

Inventories/Sales

Cash/Assets

Debt/Assets